As you begin working with financial institutions to secure your money and process your financial transactions, it is important that you learn to keep good financial records. These records, both on paper and electronic, will allow you to know where your money and assets are and exactly how much you have at a given time.

You may choose to print these documents and keep them in a binder or organize them in folders on your computer. The method used does not matter. What does matter is that you understand what is happening with your finances and know where to find the information when needed.

Financial Planning

When you are building or evolving your financial plans and setting new financial goals, you need to start with accurate financial records. Your financial documents allow you to know exactly where you are today and they will help you see when you have reached your goals

Taxes

Most people appreciate having good financial records when it comes time to file tax returns. Many thinks you spend money on throughout the year, like your car registration renewal, work uniforms, and certain types of interest on loans, can all be deducted from your taxes – but only if you have kept good records of all of those payments.

Types of Financial Records

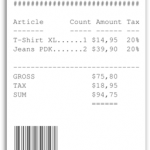

Receipts

In order to claim any deductions on your taxes, the IRS will want to see proof that specific purchases or payments were made. And in order to show proof, you will need to provide a receipt.

You should always save the receipts for large purchases (like your car’s bill of sale). Many cities also provide tax breaks if you use public transit, so it is also a good idea to save those receipts.

Getting in the habit of keeping your receipts can help you in other areas of your life as well. For example, utility bills and receipts are often required as a “proof of address” when you want to open a bank account. If you get in a conflict at a later date over a bill being paid, having a receipt can shut down the problem immediately, while proving otherwise can be a long and drawn-out process.

Bank Records

Your bank account will be one of your most important sources for financial records. Usually, your entire transaction history is saved for a few years (including every check you write), along with your current account balances. If you do not have a receipt for a payment (for example, if you write a rent check every month), you can still have a record of that transaction in your bank account.

The type of information contained in your bank records depends on the type of account you have. For example, if you have a savings account, you might have more records on deposit amounts and dates, with accumulated compound interest. If you have a checking (or “Current”) account, you will have your current available balances, along with your transaction history of your checks, debit card transactions, and ATM withdrawals. Your bank records will be an invaluable resource when you are building and changing your Spending Plan.

Income Reports

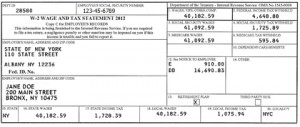

Every time you get paid, your employer creates a paycheck transaction that shows how many hours you worked, how much you get paid per hour, and the amount of money deducted from your pay for various taxes. At the end of the calendar year, your employer summarizes all of your pay information into a form known as a W-2 (or 1099, depending on your type of job) or Income Report. Outside the United States, the report has different names, but always has the same basic information.

Your income reports are statements showing how much money you’ve earned, usually along with how much income tax and social security you have paid, in a given year. These are necessary to file your taxes, but are also useful to see how your income evolves over time.

Investment Statements

If you have any stocks, bonds, or other investments, you will also get regular account statements from your broker. This will include your cash balances (available for withdrawal or purchasing more securities), the total net market value of your portfolio, the amount of any dividends you have received, and the total expenses of your investments (this is most important with mutual funds). Your investment statements are essential for tax purposes. You are legally required to report any investment income you receive, so having ready access to these documents will be essential.

Personal Property Inventory

Unlike the other primary records, this is one you will make and maintain yourself. Your personal property inventory is basically a list of what you own, where it is located, and its estimated value. This seems fairly simple when you are still in school, but there are more than a few reported cases of large amounts of cash stashed and forgotten. Your personal property inventory is not used for taxes.

The main benefit of keeping and maintaining a personal property inventory is purely organization. Knowing exactly where your things are and how much they are worth can be very useful when your life circumstances change and you want to sell (or give away) things you no longer use or might have forgotten about. The self-service storage locker industry thrives on people making monthly payments to save things they do not regularly use!

Income Tax Returns

After you’ve filed your income tax return, keep a copy for later reference. Legally you should hold on to all tax returns and receipts for 7 years, but it can be useful to keep them for longer if you want to occasionally work on long-term financial planning.

Personal Expense Records

You might end up accumulating dozens of receipts in a relatively short period of time. Every few months, try to group them together and keep them in a safe place (for example, all receipts for “January – March 2016” kept in a folder in a fire-proof safe). While you do this, copy the amounts and the reason for the purchase into an excel spreadsheet. This will make it easy to know how much you spent and where you spent it. Plus, you can use your spreadsheet to quickly and easily find the original receipt later if you need it. By filing away all your receipts regularly, you make it less likely for any to get lost or accidentally thrown out. Making this a regular habit will also help you avoid having to spend an entire afternoon sorting through and organizing your receipts.

Keeping Your Records Secure

Now that you have all of this information, your main concern is keeping it safe. Identity theft is a major problem, and if someone were to get unauthorized access to just a few of your documents, they might be able to use that information to harm you.

Storing Paper Documents

For things like your tax returns, receipts, and investment statements, you might have paper copies that need to be both easy to find and secure. One possible route is to buy a small safe you can bolt to the floor, keeping your documents safe and all in one place. Banks offer safety deposit boxes where you can safely store documents and items. Small boxes typically cost about $60 a year. The inconvenience of having to visit the bank to get access to your documents may be offset by knowing the documents are in a secure location.

Storing Electronic Documents

Keeping your computer files safe from hackers and phishers is a much more challenging prospect. There are dozens of ways to keep your records safe, but these are the most common rules to follow:

Rule #1: Don’t Share Your Login Information

Despite what the movies show, most “hacking” is done not by forcing complex computer algorithms to hack a mainframe, but usually just because someone shares a password with someone they shouldn’t have. This goes not just for passwords, but other information as well. NEVER give your account numbers, credit card numbers, usernames, or passwords over the phone or by email. If you absolutely need to share a username and/or password (sharing an account with a group, for example), make sure it is a username and password you don’t use on any other websites.

Rule #2: Don’t Re-Use Your Password

When you are on the computer, you can’t tell which sites you use let the administrators see your password, and which use proper encryption. If you re-use the same usernames and passwords in many places, you’re increasing the chances that a disgruntled co-worker steals data and breaks into your other accounts.

Rule #3: Change Your Passwords Often

Even the most secure, unique password in the world is vulnerable to keyloggers – a type of virus software that records every key you press, and reports it back to the virus’s creator. Even if you don’t have a keylogger on your home computer (which can be hidden for months or years before “activated”), it is possible one might be installed on a computer in a computer lab or on a public computer. Changing your passwords every few months is a good way to keep them safe.

Rule #4: Pick Hard-To-Guess Passwords

When you choose a password for an account, try to choose letter, symbol, and number combinations that are easy enough for you to remember but difficult for your best friend or a hacker using random letter combinations to guess. Remember, you need to do your part to keep your passwords secure.

Other Financial Record Tips and Tricks

See What Account Management Services Some Financial Institutions Can Provide

If keeping track of everything is a daunting prospect, see what kinds of services your bank or other financial institution can “bundle together”. For example, it is extremely common for a person to have their savings and checking accounts, investment portfolio, home mortgage, and credit card all through the same bank, and so they are able to access all of those financial records through the bank’s online portal.

This has a strength of convenience, but there are also some serious drawbacks. For example, if you have your password stolen for this online banking service, you might lose access to everything all at once, causing a massive headache and potentially tens of thousands of dollars.

Visit Tax Professionals or Financial Advisers

Even if you do not do it every year, taking time to visit with a professional can save you time and money in the long run. Tax professionals and financial advisers understand tax codes, investment strategies, financial pitfalls, and red tape that you may not be familiar with. Paying for their expertise may minimize how much time and research you need to spend trying to understand your financial records on your own.

You might be able to remember the basics – if you have an expense that is used primarily for business, you can probably claim a tax credit on it. However, you might not know the exact process of claiming time you used your car while working, or if you can claim sales tax exemptions for new renovations on your home. Meeting with a tax professional or a financial adviser is the easiest way to navigate the seas of red tape and get the most out of your tax returns, and minimize how much time and research you need to spend on your financial records out of your own free time.

Pop Quiz

[qsm quiz=56]