| Earning Income | | | | | | |

| Compensation for a job or career can be in the form of wages, salaries, commissions, tips, or bonuses, and may also include contributions to employee benefits, such as health insurance, retirement savings plans, and education reimbursement programs. | Lesson – What’s in Your Compensation Package?Lesson – Planning Your Career Path | | | | | |

| In addition to wages and paid benefits, employees may also value intangible (non�cash) benefits, such as good working conditions, flexible work hours, telecommuting privileges, and career advancement potential. | Lesson – What’s in Your Compensation Package?Lesson – Planning Your Career PathLesson – The Ultimate Employee Guide | | | | | |

| People vary in their opportunity and willingness to incur the present costs of additional training and education in exchange for future benefits, such as earning potential. | Lesson – Go to College or Start Working?Lesson – Planning Your Career Path | | | | | |

| Employers generally pay higher wages or salaries to more educated, skilled, and productive workers than to less educated, skilled, and productive workers. | Lesson – Planning Your Career PathLesson – Why Do Some Jobs Pay More Than Others? | | | | | |

| Changes in economic conditions, technology, or the labor market can cause

changes in income, career opportunities, or employment status. | Lesson – The Business CycleLesson – Why Do Some Jobs Pay More Than Others?Lesson – Inflation | | | | | |

| Federal, state, and local taxes fund government-provided goods, services, and transfer payments to individuals. The major types of taxes are income taxes, payroll taxes, property taxes, and sales taxes. | Lesson – Tax Basics You Need to KnowLesson – Sales Tax: Who Pays, Collects, and Why?Lesson – Tax Credits & Deductions You Need to KnowLesson – What Is Monetary Policy? | | | | | |

| The type and amount of taxes people pay depend on their sources of income, amount of income, and amount and type of spending. | Lesson – Tax Basics You Need to KnowLesson – Sales Tax: Who Pays, Collects, and Why?Lesson – Tax Credits & Deductions You Need to KnowLesson – Uncovering Hidden Income Taxes You OweLesson – Do You Need a Tax Professional? | | | | | |

| Interest, dividends, and capital appreciation (gains) are examples of unearned income derived from financial investments. Capital gains are subject to different tax rates than earned income. | Lesson – Tax Basics You Need to KnowLesson – Income Tax Filing Tips and Tricks | | | | | |

| Tax deductions and credits reduce income tax liability. | Lesson – Tax Credits & Deductions You Need to Know | | | | | |

| Retirement income typically comes from some combination of continued employment earnings, Social Security,employer sponsored retirement plans, and personal investments. | Lesson – The Secret to a Comfortable RetirementLesson – What is Wealth? | | | | | |

| Owning a small business can be a person’s primary career or can supplement income from other sources | Lesson – Starting a Business 101Lesson – What is Entrepreneurship? | | | | | |

| Spending |

Activity |

Long-Term Game |

Comprehensive Chapter |

Short Lesson |

Interactive Calculator |

Graded Assessment |

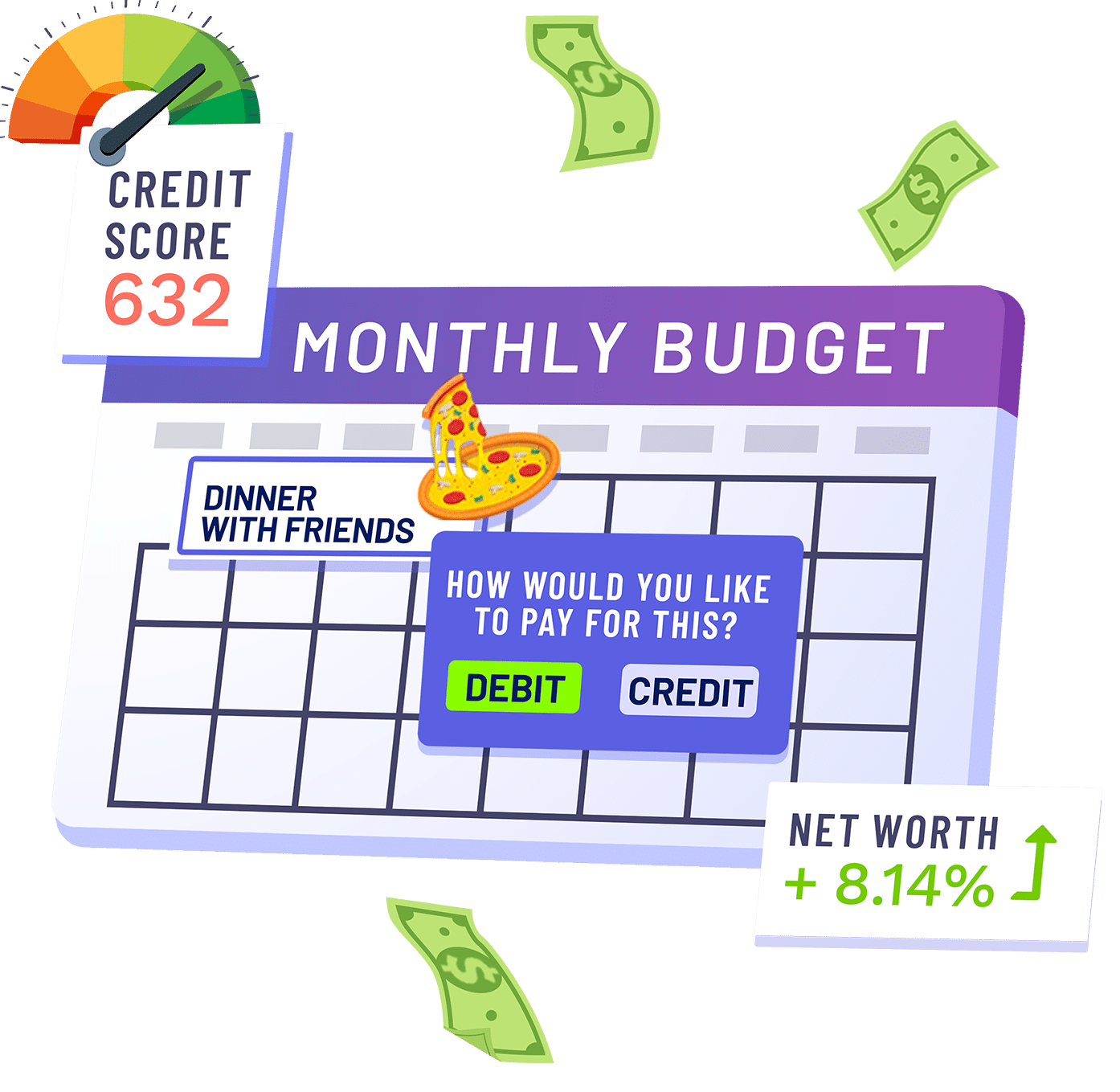

| A budget helps people achieve their financial goals by allocating income to necessary and desired spending, saving, and philanthropy. | Budget Game – Core ComponentLesson – Lesson – Break Free From Money Stress with a BudgetLesson – Pay Yourself First: A Simple Yet Powerful Way to Build WealthLesson – Achieve Financial Goals with a Spending Plan | | | | | |

| Consumer decisions are influenced by the price of products or services, the

price of alternatives, the consumer’s budget and preferences, and potential impact on the environment, society, and economy. | Budget Game – Core ComponentLesson – Lesson – Break Free From Money Stress with a BudgetLesson – Proven Techniques to Stop OverspendingLesson – Achieve Financial Goals with a Spending PlanLesson – How Do You Stop Impulse Purchases?Lesson – Benefits of CompetitionLesson – Analyzing Consumer Behavior | | | | | |

| When purchasing a good that is expected to be used for a long time, consumers consider the product’s durability, maintenance costs, and various product features. | Lesson – Evaluating Big-Ticket Purchases | | | | | |

| Consumers may be influenced by how prices of goods and services are advertised, and whether prices are fixed or negotiable. | Lesson – Analyzing Consumer BehaviorLesson – Foundations of MarketingLesson – Achieve Financial Goals with a Spending PlanLesson – Why You Buy What You Buy | | | | | |

| Consumers incur costs and realize benefits when searching for information related to the purchase of goods and services. | Lesson – How Do You Stop Impulse Purchases?Lesson – Protect Yourself as a Consumer | | | | | |

| Housing decisions depend on individual preferences, circumstances, and costs, and can impact personal satisfaction and financial well-being | Budget Game – Core ComponentLesson – The Cost of Raising a FamilyActivity – Rent or Buy: Which is Right for You? | | | | | |

| People donate money, items, or time to charitable and non-profit organizations because they value the services provided by the organization and/or gain satisfaction from giving. | Lesson – A Guide to Effective Charitable Donations | | | | | |

| Federal and state laws, regulations, and consumer protection agencies (e.g., Federal Trade Commission, Consumer Affairs office, and Consumer Financial Protection Bureau) can help individuals avoid unsafe products, unfair practices, and marketplace fraud. | Lesson – Protect Yourself as a ConsumerLesson – Ethics In Marketing | | | | | |

| Having an organized system for keeping track of spending, saving, and investing makes it easier to make financial decisions. | Lesson – Tame Your Financial PaperworkLesson – Balance Your Books in 10-MinutesLesson – Lesson – Break Free From Money Stress with a Budget | | | | | |

| Saving |

Activity |

Long-Term Game |

Comprehensive Chapter |

Short Lesson |

Interactive Calculator |

Graded Assessment |

| Financial institutions offer several types of savings accounts, including regular savings, money market accounts, and certificates of deposit (CDs), that differ in minimum deposits, rates, and deposit insurance coverage. | Lesson – Choosing the Best Banking Option for YouLesson – How to Develop an Investing Strategy | | | | | |

| Deposit account interest rates and fees vary between financial institutions and depend on market conditions and competition. | Lesson – Choosing the Best Banking Option for You | | | | | |

| Unless offered by insured financial institutions, mobile payment accounts and cryptocurrency accounts are not federally insured and usually do not pay interest to depositors. | Lesson – Choosing the Best Banking Option for YouInvesting101 Course – Chapter 8: Current Hot Topics In Trading | | | | | |

| Inflation can erode the value of savings if the interest rate earned on a savings account is less than the inflation rate. | Lesson – Inflation | | | | | |

| Government agencies such as the Federal Reserve, the FDIC, and the NCUA, along

with their counterparts in state government, supervise and regulate financial institutions to improve financial solvency, legal compliance, and consumer protection. | Lesson – Why You Should Care About the FedLesson – Choosing the Best Banking Option for You | | | | | |

| Tax policies that allow people to save pretax earnings or to reduce or defer taxes on interest earned provide incentives for people to save. | Lesson – What Is Monetary Policy? | | | | | |

| Employer defined contribution retirement plans and health savings accounts can provide incentives for employees to save. | Lesson – The Secret to a Comfortable RetirementLesson – What’s in Your Compensation Package? | | | | | |

| People can reduce the potential for future financial strife with a partner or spouse by sharing personal financial information, goals, and values prior to combining finances. | Lesson – The Cost of Raising a Family | | | | | |

| There are many strategies that can help people manage psychological, emotional, and external obstacles to saving, including automated savings plans, employer matches, and avoiding personal triggers. | Lesson – Achieve Financial Goals with a Spending PlanLesson – Pay Yourself First: A Simple Yet Powerful Way to Build Wealth | | | | | |

| Investing |

Activity |

Long-Term Game |

Comprehensive Chapter |

Short Lesson |

Interactive Calculator |

Graded Assessment |

| A person’s investment risk tolerance depends on factors such as personality, financial resources, investment experiences, and life circumstances. | Lesson – Knowing Your Risks and Risk ToleranceLesson – How to Develop an Investing StrategyInvesting101 Course – Chapter 1: Introduction to Investing | | | | | |

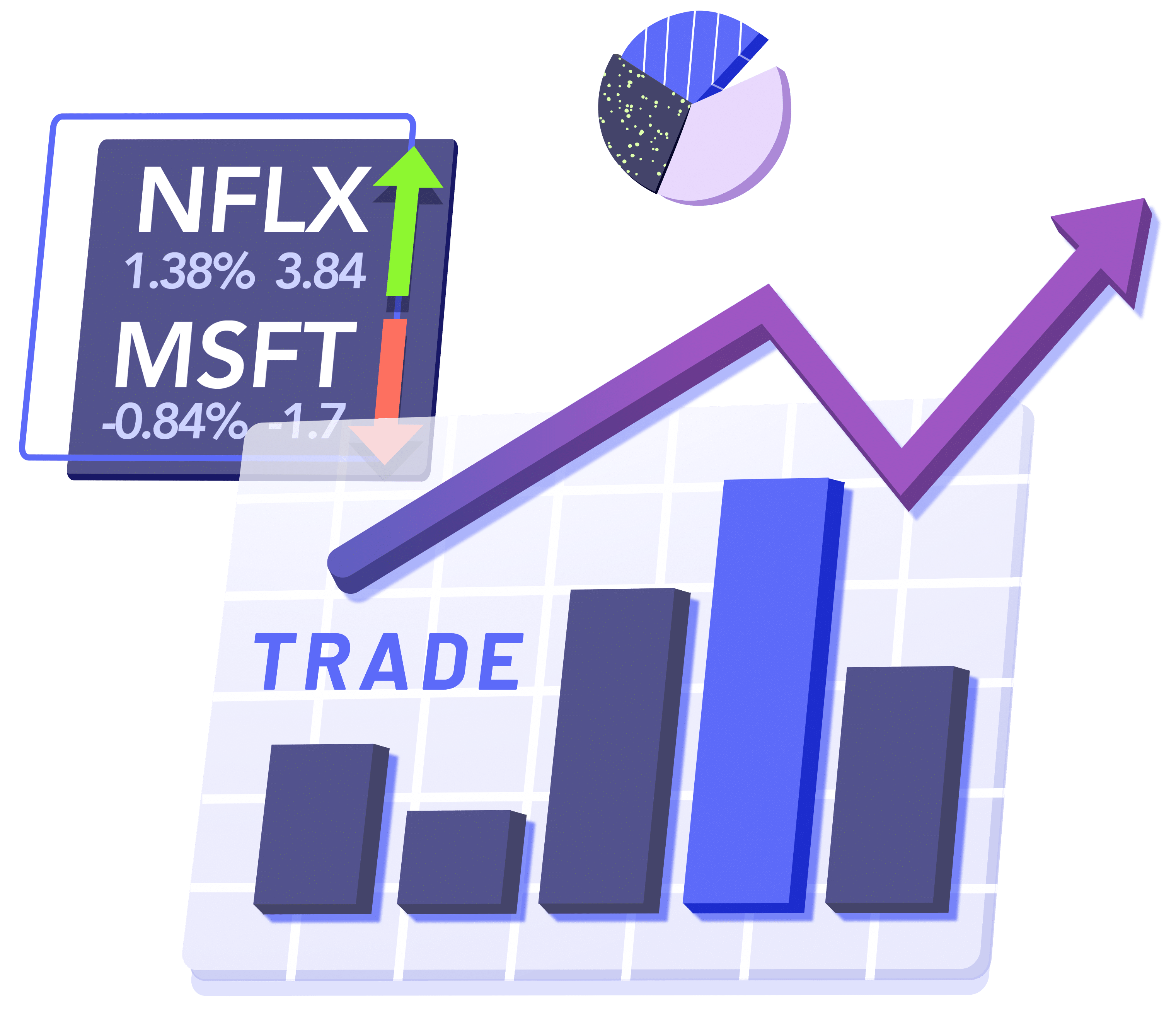

| Investors earn investment returns from price changes and annual cash flows (such as interest, dividends or rent).The nominal annual rate of return is the annual total dollar benefit as a percentage of the beginning price. | Activity – Model Your Financial FutureInvesting101 Course – Chapter 1: Introduction to Investing | | | | | |

| Investors expect to earn higher rates of return when they invest in riskier assets. | Stock Game – Core ComponentActivity – Model Your Financial FutureLesson – How to Develop an Investing StrategyLesson – Knowing Your Risks and Risk Tolerance | | | | | |

| Because inflation reduces purchasing power over time, the real return on a financial asset is lower than its nominal return. | Lesson – InflationActivity – Model Your Financial Future | | | | | |

| The prices of financial assets change in response to market conditions, interest rates, company performance, new information, and investor demand. | Lesson – Decoding What Moves The MarketInvesting101 – Chapter 6: Fundamental Analysis: Understanding Earnings and Cash FlowChapter 7: Technical Analysis: Common Charts and Terms | | | | | |

| When making diversification and asset allocation decisions, investors consider their risk tolerance, goals, and investing time horizon. | Lesson – How to Develop an Investing StrategyLesson – What is Diversification and How to Spread Your Risk | | | | | |

| Expenses of buying, selling, and holding financial assets decrease the rate of return from an investment. | Stock Game – Core ComponentActivity – Model Your Financial FutureInvesting101 – Chapter 5: Now That I Own It, What Should I Do? | | | | | |

| Tax rules affect the rate of return on different investments, and can vary by holding period, type of income, and type of account | Lesson – Tax Basics You Need to Know | | | | | |

| Common behavioral biases can result in investors making decisions that adversely affect their investment outcomes | Lesson – 5 Ways to Get Investing IdeasLesson – How to Choose Stocks StrategicallyLesson – Decoding What Moves The MarketInvesting101 – Chapter 1: Introduction to Investing | | | | | |

| Financial technology can counterbalance negative behavioral factors when making investment decisions | Lesson – How to Develop an Investing StrategyLesson – How to Choose Stocks Strategically | | | | | |

| Many investors buy and sell financial assets through discount brokerage firms that provide inexpensive investment services and advice using financial technology. | Lesson – Finding the Right Brokerage Account | | | | | |

| Federal regulation of financial markets is designed to ensure that investors have access to accurate information about potential investments and are protected from fraud. | Lesson – Knowing Your Risks and Risk ToleranceLesson – How to Avoid Identity Theft, Scams and FraudLesson – Could the 1929 Crash Happen Again? | | | | | |

| Investors often compare the performance of their investments against a benchmark, such as a diversified stock or bond index. | Stock Game – Core ComponentInvesting101 – Chapter 3: Making Your First Trade | | | | | |

| Criteria for selecting financial professionals for investment advice include licensing, certifications, education, experience, and cost. | Lesson – Want to Work in Finance?Lesson – Do You Need a Tax Professional? | | | | | |

| Managing Credit |

Activity |

Long-Term Game |

Comprehensive Chapter |

Short Lesson |

Interactive Calculator |

Graded Assessment |

| Borrowers can compare the cost of credit using the Annual Percentage Rate (APR) and other terms in the loan or credit card contract. | Lesson – A Beginner’s Guide to Borrowing WiselyLesson – Credit Cards: Terms, Fees, and More | | | | | |

| Loans that are secured by collateral have lower interest rates than unsecured loans because they are less risky to lenders. | Lesson – A Beginner’s Guide to Borrowing WiselyLesson – Mortgage Options for First-Time HomebuyersLesson – How to Use Debt to Your Advantage | | | | | |

| Monthly mortgage payments vary depending on the amount borrowed, the repayment period, and the interest rate, which can be fixed or adjustable. | Lesson – Mortgage Options for First-Time HomebuyersActivity – Find Out Your Monthly Home Budget | | | | | |

| Post-secondary education is often financed by students and families/caregivers through a combination of scholarships, grants, student loans, work-study, and savings. | Lesson – Financing Your EducationLesson – Go to College or Start Working? | | | | | |

| Federal student loans have lower rates and more favorable repayment terms than private student loans, and may be subsidized. | Lesson – Financing Your EducationLesson – How to Use Debt to Your Advantage | | | | | |

| Down payments reduce the amount needed to borrow. | Lesson – The Car Buying ChecklistActivity – Calculate Your Car Loan PaymentsActivity – Find Out Your Monthly Home Budget | | | | | |

| Lenders assess credit-worthiness of potential borrowers by consulting credit reports compiled by credit bureaus. | Lesson – What Your Credit Report Says About You | | | | | |

| A credit score is a numeric rating that assesses a person’s credit risk based on information in their credit report. | Budget Game – Core ComponentLesson – What Your Credit Report Says About You | | | | | |

| Credit reports and credit scores may be requested and used by entities other than lenders. | Lesson – What Your Credit Report Says About You | | | | | |

| Borrowers who face negative consequences because they are unable to repay their debts may be able to seek debt management assistance. | Lesson – Getting Help With Debt RepaymentLesson – How to Negotiate With Creditors | | | | | |

| In extreme cases, bankruptcy may be an option for people who are unable to repay their debts. | Lesson – What Is Bankruptcy? | | | | | |

| Consumer credit protection laws govern disclosure of credit terms, discrimination in borrowing, and debt collection practices. | Lesson – Credit Cards: Terms, Fees, and MoreLesson – Protect Yourself as a Consumer | | | | | |

| Alternative financial services, such as payday loans, check�cashing services, pawnshops, and instant tax refunds, provide easy access to credit, often at relatively high cost. | Lesson – What to Do When You Need Money FastLesson – How to Use Debt to Your Advantage | | | | | |

| Managing Risk |

Activity |

Long-Term Game |

Comprehensive Chapter |

Short Lesson |

Interactive Calculator |

Graded Assessment |

| People vary with respect to their willingness to accept risk and in how much they are willing to pay for insurance that will allow them to minimze future financial loss. | Lesson – Knowing Your Risks and Risk ToleranceLesson – Life Insurance: The Ultimate Safety Net | | | | | |

| The decision to buy insurance depends on perceived risk exposure, the price of insurance coverage, and individual characteristics such as risk attitudes, age, occupation, lifestyle, and financial profile. | Lesson – What’s Not Covered in Renter’s Insurance?Lesson – Car Insurance: How to Lower Your RatesLesson – Why Health Insurance is So Expensive | | | | | |

| Some types of insurance coverage are mandatory. | Lesson – Car Insurance: How to Lower Your RatesLesson – Why Health Insurance is So Expensive | | | | | |

| Insurance premiums are lower for people who take actions to reduce the likelihood and/or financial cost of losses and for those who buy policies with larger deductibles or copayments. | Lesson – Car Insurance: How to Lower Your RatesLesson – Why Health Insurance is So ExpensiveLesson – What Damage Does Home Insurance Cover? | | | | | |

| Health insurance provides coverage for medically necessary health care and may also cover some preventive care. It is sometimes offered as an employee benefit with the employer paying some or all of the premium cost. | Lesson – Why Health Insurance is So ExpensiveLesson – The Ultimate Employee GuideLesson – What’s in Your Compensation Package? | | | | | |

| Disability insurance replaces income lost when a person is unable to earn their regular income due to injury or illness. In addition to privately purchased policies, some government programs provide disability protection. | Lesson – Why Health Insurance is So Expensive | | | | | |

| Auto, homeowner’s and renter’s insurance reimburse policyholders for financial losses to their covered property and the costs of legal liability for their damages to other people or property. | Lesson – What’s Not Covered in Renter’s Insurance?Lesson – Car Insurance: How to Lower Your RatesLesson – What Damage Does Home Insurance Cover? | | | | | |

| Life insurance provides funds forbeneficiaries in the event of an insured person’s death. Policy proceeds are intended to replace the insured’s lost wages and/or to fund their dependents’ future financial needs. | Lesson – Life Insurance: The Ultimate Safety Net | | | | | |

| Unemployment insurance, Medicaid, and Medicare are public insurance programs that protect individuals from economic hardship caused by certain risks. | Lesson – The Anatomy of Unemployment | | | | | |

| Insurance fraud is a crime that encompasses illegal actions by the buyer (e.g., falsified claims) or seller (e.g., representing non-existent companies) of an insurance contract. | Lesson – Life Insurance: The Ultimate Safety Net | | | | | |

| Online transactions and failure to safeguard personal documents can make consumers vulnerable to privacy infringement, identity theft, and fraud. | Lesson – How to Avoid Identity Theft, Scams and Fraud | | | | | |

| Extended warranties and service contracts are like an insurance policy. | Lesson – Protect Yourself as a Consumer | | | | | |