Picture this – you are a student playing through the PersonalFinanceLab budgeting game, and you get a prompt – do you want to buy an aquarium? The cost is $100. In the real world, tons of people buy aquariums – it is a personal preference, but maybe you really like looking at fish. This is Read More…

You’ve got an important announcement for your students. Maybe you already posted it to your classroom page, and sent out an email. Even wrote it on the board in class. But if you want to be extra sure they see it, you also want to pop it in front of them while they’re working through Read More…

You’re planning to use the PersonalFinanceLab stock game in your class. You’ve used stock games before, and have seen some students buy something in the first week, then forget about it until the end of the semester. You want to encourage students to keep an eye on their portfolio, and re-balance it over time, just Read More…

Did It Work? That is the biggest question teachers need to know after using any resource in the classroom – did it actually improve outcomes? And we at PersonalFinanceLab could not agree more. That is why a year ago we implemented our Pre- and Post- tests as part of our Assignments engine, allowing teachers to Read More…

Stash101 shuts down as a money management and investment simulation for schools, with all existing accounts disabled on January 31, 2023. What happened to Stash101? Stash is primarily a banking app, which also can include a personal checking account. Stash101 was a free “practice” version with other educational resources built in, designed for schools and Read More…

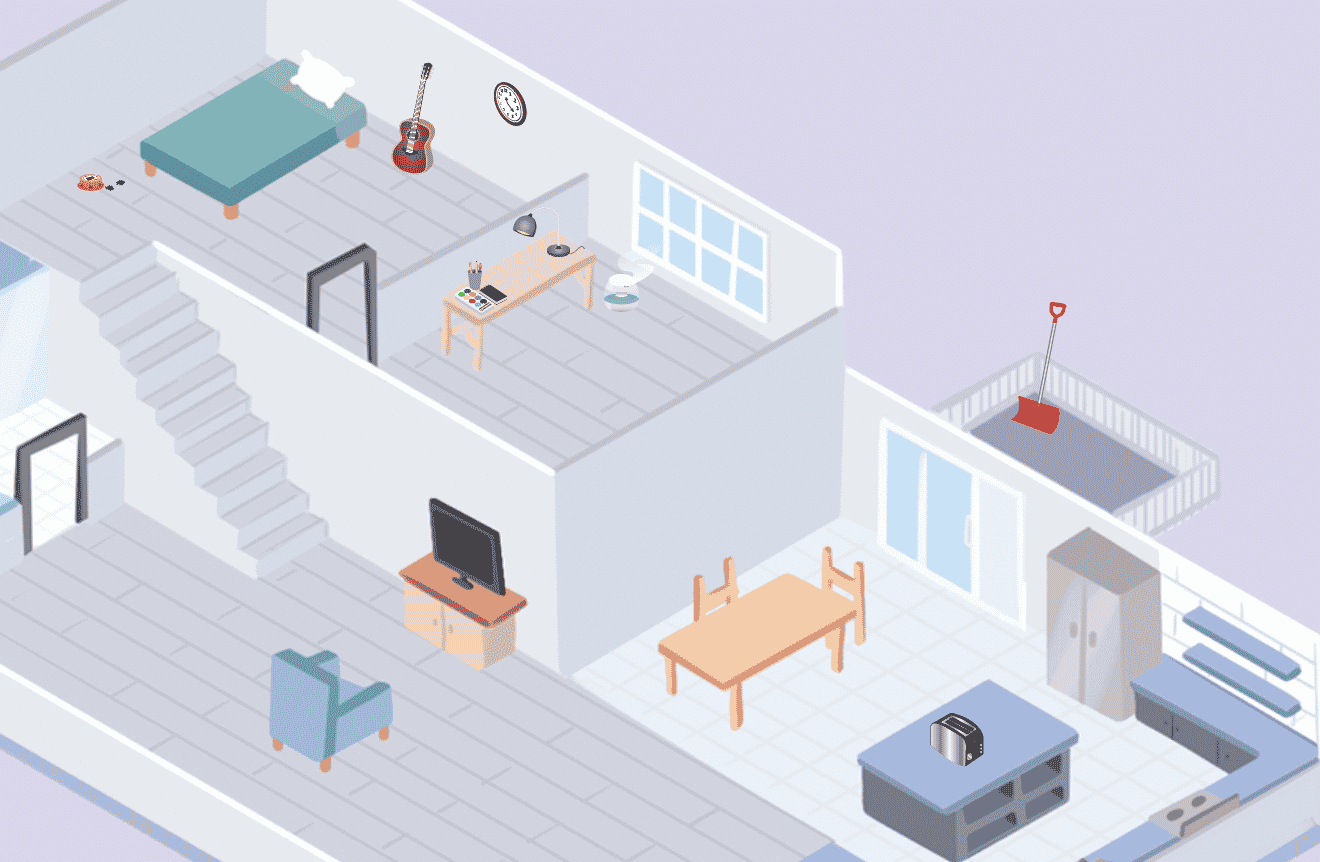

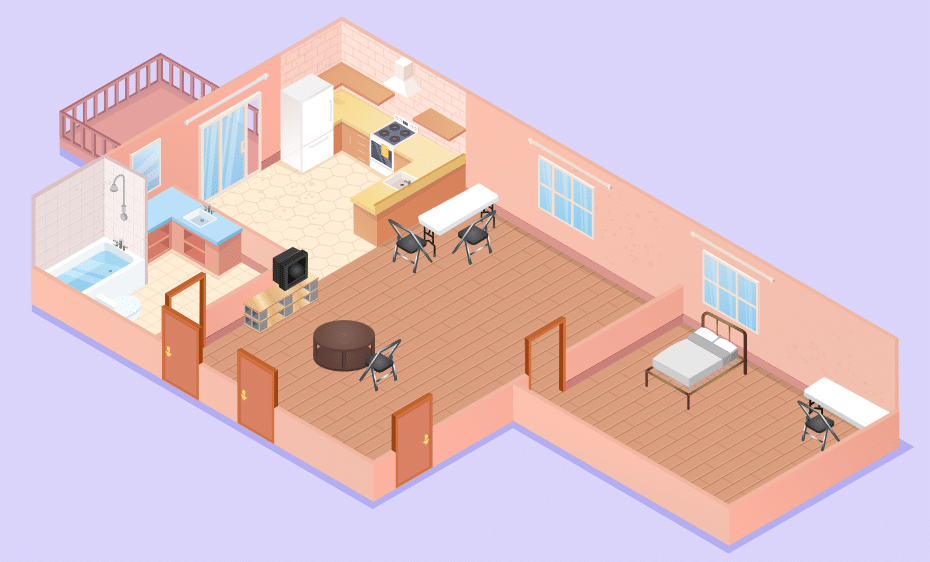

For Spring 2023, we have one of the most exciting additions we’ve ever seen to the PersonalFinanceLab Budget Game! One of the most consistent items of feedback we get from students every semester in our budget game was that most events of the game had no long-term visual impact – a choice to buy an Read More…

Gamification has been a buzzword in education for over a decade. Teachers now have access to more games for the classroom than ever, with a dizzying array of options to fill a limited number of weeks in the classroom. To try to help teachers pick out the best possible options for your students, we want Read More…

Hey teachers – we have a major update in store for you this Fall! From budget game graphics updates to currency trading and everything in between, this might be our biggest update ever! Clever Integration We are making it easier than ever to get students registered into your class! Starting this Fall, teachers can add Read More…

Introduction This course outline is designed for condensed learning programs for financial literacy, usually taking place over the summer. Enrichment programs can vary in length, but our benchmark for pacing is a 3-week program that meets for approximately 2 hours a day, 5 days a week. With student packets that can be easily shared with Read More…

This course outline is designed for a 9-week Personal Finance Class. It makes heavy use of PersonalFinanceLab’s Budget and Stock Games, as well as our Learning Library with self-grading assessments to measure student progress. Notice for teachers joining our Free Financial Literacy Events – Our free events do not have full admin access for teachers Read More…

Coming to Personal Finance Lab Spring 2021 There are a lot of new enhancements that will be coming this January and will improve how both teachers and students use the platform. Quick Overview Stock Game Weekly Deposits $1 Starting Cash Budget Game Starting Positions Graphics Update System Updates New Badges New Widgets New Certifications New Read More…

What is a Student Loan? A student loan is exactly what it sounds like – a loan given to students to finance their studies. This is most common for college or university students, but also works for trade schools and other vocational studies. Most of the time when a person takes out a loan, they Read More…

If you have used a stock game in your class before, you know the drill – you choose your class’s custom rules and starting cash (usually around $100,000), your students sign in, and they use that cash to build their portfolio that they manage over the course of a semester. This might make sense to Read More…

PersonalFinaceLab’s curriculum library is packed full of automatically-graded quizzes and assessments at the end of every lesson. However, to give students an additional push, you may also want to assign students open-ended questions for short written assignments, or launching points for class discussion. Most of our Personal Finance lessons end with 4-6 “Challenge Questions” – Read More…

Our latest teacher webinar walks through some of the basics of gamification – and the keys to best leverage these new levels of engagement to supercharge your blended and remote classrooms this Fall! If you are using a blended or fully-remote classroom, quality online resources are more important than ever! Our new Badges and Achievement Read More…

With the next major update to the PersonalFinanceLab Budget Game, your students can graduate from school and start their Full Time Jobs! How It Works If you have used the Budget Game before, your class would have taken on the role of college students with a part-time job. They would be working variable hours each Read More…

This Summer, PersonalFinanceLab has partnered with BountyBlok to power our awesome new Badges and Achievement system to bring classroom engagement to a whole new level! Personal Finance should never be boring for students – by working with BountyBlok, our Assignments engine is supercharged with new ways to track student activity and provide them with real-time Read More…

Our first major enhancement of the summer is almost here! The next release of Personal Finance Lab focuses on our Assignments – our awesome system used to manage curriculum and track your students’ progress through our Stock Game and Budget Game. There’s three game-changing new features you can expect for your next classes: Rewards, Prerequisites, Read More…

If you find yourself teaching a class remotely for the first time this Spring, never fear! PersonalFinanceLab.com has everything you need for a knock-out distance learning class, all in one place. Our engaging simulations, interactive games, built-in assessments, multi-media curriculum, customizable lesson plans, and teacher presentation and video library has everything you need to turn Read More…

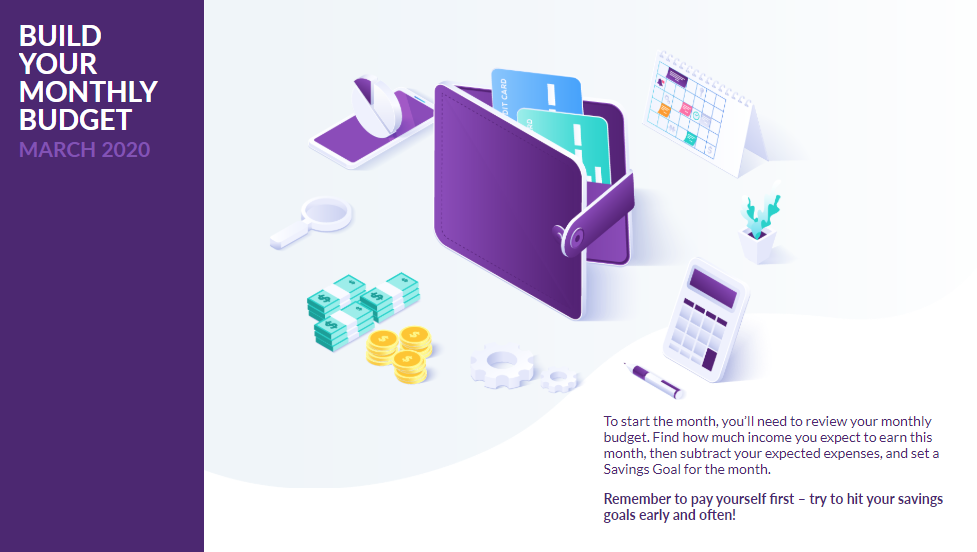

Just in time for March, the Personal Finance Lab team is excited to announce a massive new update for our budgeting game! Our latest update includes some huge enhancements for your class, including: An overhaul to the Quality of Life scores, making the point scoring system much easier to understand. A new Overall Game Score, Read More…

Once you get started on progressing through your first month, you’ll notice that you have two different ways to pay for almost every expense – your Debit Card or Credit Card. Understanding the two, and how to use them, will be essential to effectively managing your budget. Your Debit Card Making a purchase with your Read More…

Very few students will ever care to know how to graph a parabola, but everyone will need to know how to do their taxes. Don’t require trigonometry but require basic tax preparation. Lindsey, 41, mixed race mother of five in Oregon suburb Personal Finance Lab’s parent organization turns 30 this year, and we have been Read More…

This presentation accompanies our lesson on Working vs Studying after high school, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Stocks, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Ticker Symbols, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Spending Plans, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Researching Purchases, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Reconciling Accounts, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Building an Investing Strategy, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Reading Stock Quotes, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Protecting Against Fraud, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Portfolio Diversification, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Planning Long-Term Purchases, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Opportunity Cost, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on filing income taxes, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Getting Trading Ideas, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Family Planning, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Using Credit, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Credit Reports, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Credit Cards, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Classifying Products and Services, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Car Insurance, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on buying a car, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Building an Investing Strategy, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Budgeting, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Budgeting and Spending Strategies, which is available as a class Assignment with a built-in assessment. Click Here to view the main lesson! Click Here to copy this presentation to Google Slides Click Here to download this presentation as a PowerPoint

This presentation accompanies our lesson on Bonds, which is also available to include in your class assignments with an assessment. Click here to view the main lesson! Copy this presentation to Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson on Payroll Accounting, which is also available to be included in your class Assignment with an assessment. Click Here to view! Copy this presentation in Google Slides Download this presentation as a PowerPoint

This presentation accompanies our lesson about Sales Tax, which is available as an “Assignment”. Copy this presentation in Google Drive Download this presentation as a PowerPoint