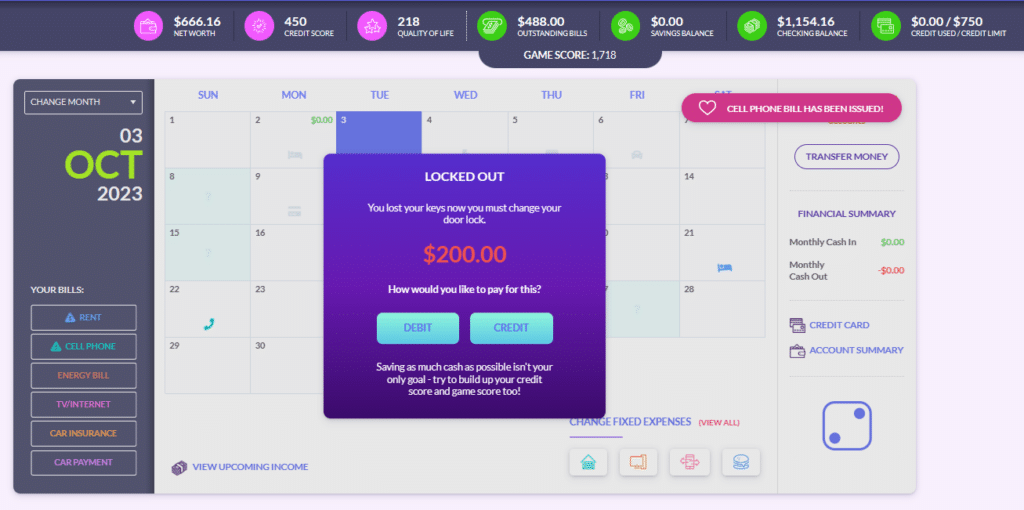

The second project of the budget game takes place after 7 months of play, immediately before beginning our unit on Careers. This timing is important – after 6 months, your students will have “graduated” from school in the game and begun their first full-time job, and so at this point students have gotten their first taste of full-time work. There are several changes to the game when the students enter “Full Time Mode”, but the most important are:

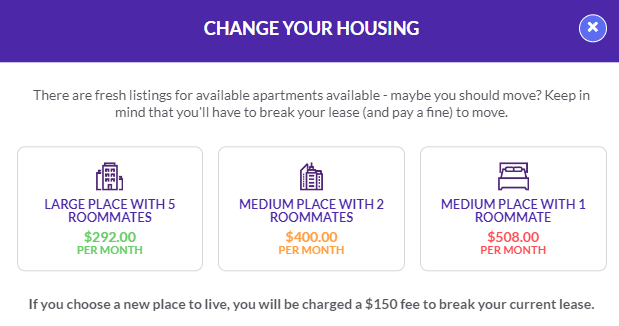

- Students move out of their old place and need to choose new, more expensive, fixed expenses (since they no longer have roommates).

- Students will now work a fixed 40 hours per week and receive their paychecks every 2 weeks instead of weekly.

- Students’ starting wage at their new job is based both on your class settings, but also by how much they “studied” in school. Students who did a lot of studying while in school will have a higher starting wage than students who did not.

- “Study” on the weekends is replaced with “Professional Development”. Conducting a lot of professional development can lead to raises at their job.

- New bills for Student Loan Payments and Health Insurance are added.

- There are new events added to the game to reflect their full-time status. Some students will have the opportunity to adopt a pet (which will improve Quality of Life but cause a permanent increase to their grocery bills) or buy a new car (which will increase their Quality of Life but cause a permanent increase to their Car Insurance and Car Payment bills).

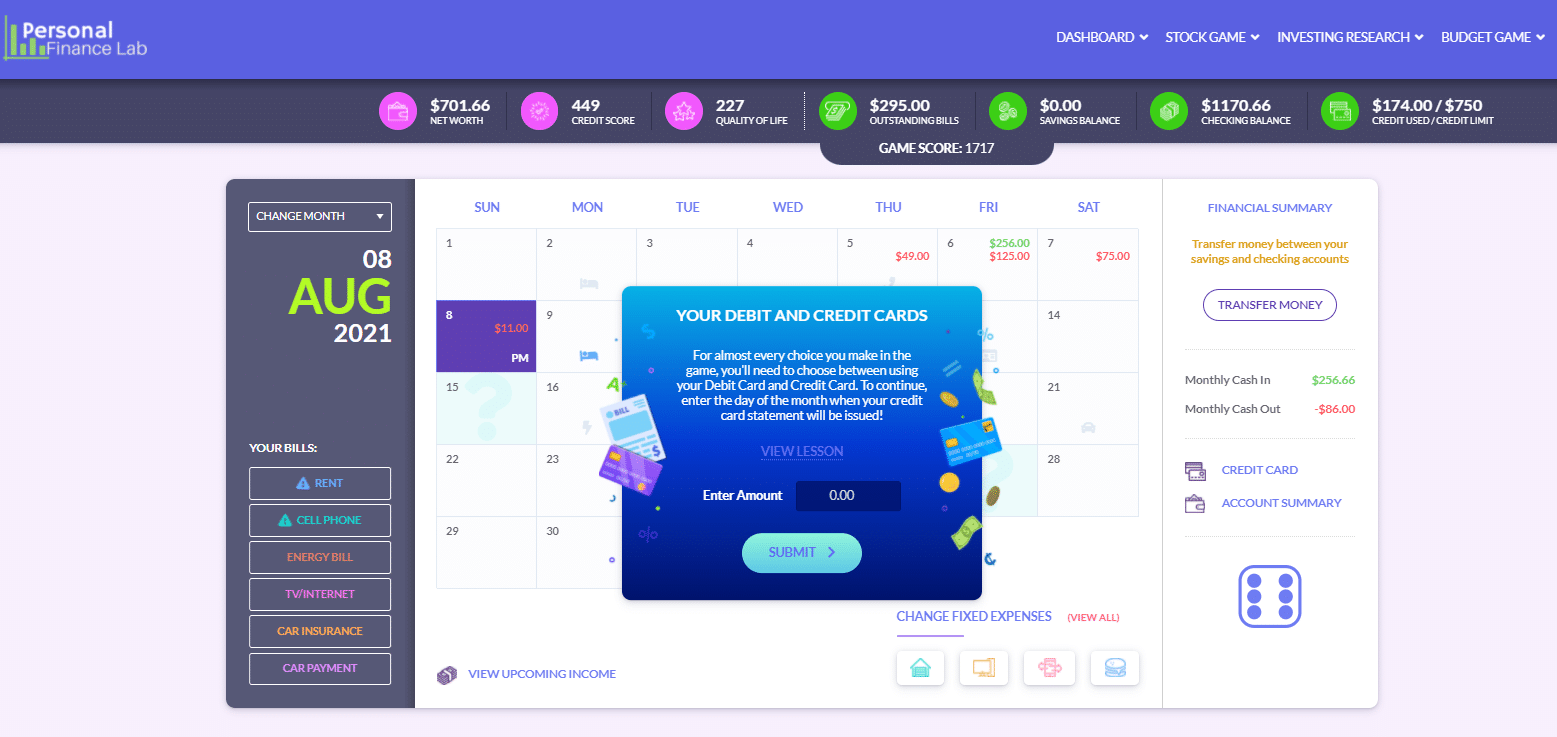

The game is generally balanced so students will have just as easy (or hard) of a time reaching a 10% savings goal each month as they did in part-time mode, but bigger expenses, new bills, and less frequent paychecks make it more difficult to manage their cash flow over the course of the month. Building a higher credit score and having a higher credit limit to help cover cash crunches becomes much more important.

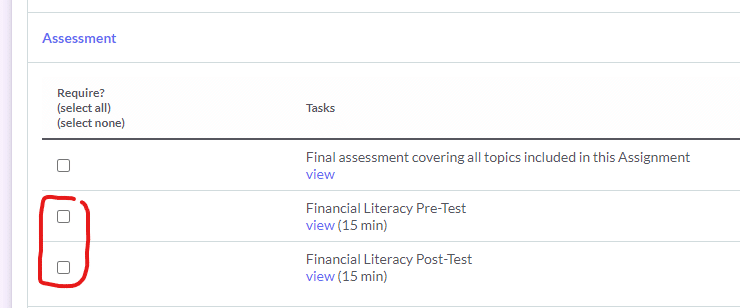

The first Budget Game activity we recommended as homework, followed up by a short discussion at the start of the next class. This activity we recommend to start with a 10 minute in-class discussion of what students noticed was different in the game once they entered full-time mode (ideally identifying a student who did a lot of “studying” before and now is earning more at their job than their peers), followed by a short 5-minute homework to write a half-page plan of how they expect to approach the game differently now that they are a full-time worker.

Evaluation is based on the creativity and insight of the student’s response based on elements they were able to pull out of the in-class discussion.

Grading Rubric

| Needs Improvement (1) | Meets Expectations (2) | Exceeds Expectations (3) | Total Score | |

| Participation | Student did not participate in-class, and the written response was missing or incomplete. | The written assignment was completed, but student did not participate in-class. | The student participated actively in the in-class discussion and submitted a complete assignment. | |

| Insight | Description of changes to the game were not in line with topics covered through the in-class discussion | Description of their new game plan incorporates elements from in-class discussion. | Description of new game plan incorporates both in-class discussion and other expectations on how the student thinks the game may continue to evolve. | |

| Style and Presentation | Answers are disorganized and difficult to follow. Numerous spelling/grammar errors. | Answers can be understood easily with minimal spelling/grammar errors. | Answers are creatively presented in an easy-to-understand format with no spelling or grammar errors |

Budget Game – Activity Rubric

The budget game is balanced students playing a “perfect game” following all financial literacy best practices should be able to:

- Set and hit a savings goal of least 10% of their income every month

- This would earn 7,200 “bonus points” through the game

- Build a $1,000 emergency fund

- This would earn 2,000 “bonus points” through the game

- Earn a total credit score of at least 780

- And accumulate at least 9,000 “Quality of Life” points.

We do not recommend student evaluation based on their final Net Worth, and this does not factor into their overall score. We do, however, include this on the class rankings page so students can see their final standing.

This would give a student playing a “perfect game” an overall score of around 30,000 points. However, because there can be a learning curve (especially in the first three months) and these scores may be different depending on the individual settings teachers make for their class, our recommended student evaluation of the game is a bit more flexible.

Grading Rubric

| Needs Improvement (1) | Meets Expectations (2) | Exceeds Expectations (3) | Total Score | |

| Completeness | Student has completed fewer than 8 months of the game | Student has completed between 8 and 11 months of the game | Student has completed all 12 months of the game on time | |

| Emergency Fund | Student finishes the game with less than $500 in their savings account as an Emergency Fund | Student finishes the game with between $501 and $999 in their savings account as an emergency fund | Student finishes the game with over $1,000 in their savings account as an emergency fund | |

| Monthly Savings Goals | Student has accumulated fewer than 3,000 “bonus points” for hitting savings goals | Student has earned between 3,000 and 8,000 “bonus points” for hitting their savings goals | Student has earned over 8,000 points through the game by setting and hitting realistic savings goals | |

| Credit Score | Student has a final credit score of less than 500 points | Student has a final credit score between 500 and 650 | Student has a final credit score above 650 | |

| Quality of Life | Student has a Quality-of-Life score less than 3,000 points | Student has a Quality-of-Life score between 3,000 and 6,000 points | Student as a Quality-of-Life score above 6,000 points |

Student Packet

Download and distribute the student packet for this activity by clicking the button below!